Originally published by Perry Williams of The Australian

28.05.2026

Fossil fuel spending in 2026 will hit its highest levels in a decade, with annual growth in renewables set to fall as the Iran war pushes Asian nations to keep coal power plants running for longer to boost energy security, the International Energy Agency said.

Coal investment is set to rise 4 per cent to $US180bn ($253bn) in 2026, the highest level since 2012.

China accounts for almost 70 per cent of global coal supply spending, with Australia the second largest contributor with several major metallurgical coal projects.

Investment in coal production in 2026 is set to increase by 5 per cent for thermal coal and 3 per cent for the steel-making raw material.

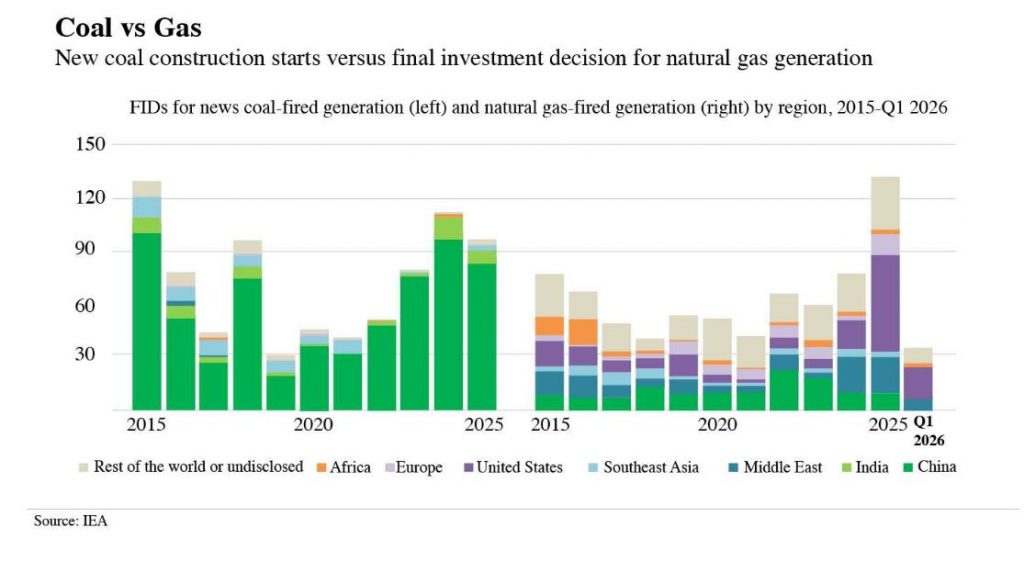

The Middle East conflict has seen a resurgence of coal as an energy security safeguard with countries especially in Asia revisiting their strategic assessment of coal’s place in their future energy mix.

“Some Asian countries affected by the current crisis may seek to keep existing coal-fired power plants operating for longer to bolster energy security,” the IEA said in its annual World Energy Investment report.

Gas investment is tipped to rise to $US330bn, the highest level in a decade, due to a wave of new LNG projects in the US and Qatar, while orders for new gas-fired power plants reached a 25-year high in 2025, driven by the AI data-centre boom sweeping the globe.

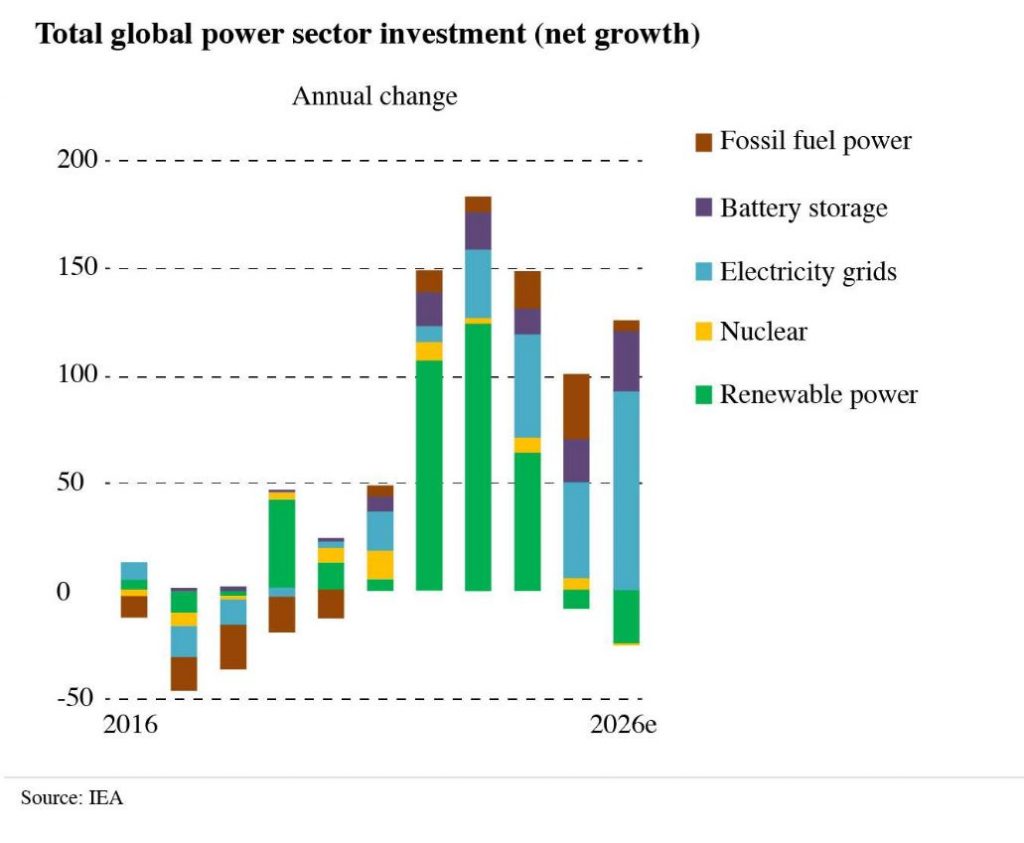

Overall global energy investment will reach $US3.4 trillion in 2026, a slight annual rise. Some $2.2 trillion will be spent on power grids, storage, low-emissions fuels, nuclear, renewables, efficiency and electrification, while around $US1.2 trillion is set to be invested in oil, gas and coal.

Annual investment growth in renewables has moderated following several years of rapid expansion.

The energy body said a smaller pipeline of renewables projects under construction combined with continued declines in equipment prices, contributed to a fall in renewables investment in 2025, which is expected to continue into 2026.

Green investment spending declined in China through 2025, which the IEA attributed to the result of steep reductions in capital costs for solar and wind rather than a “deliberate pivot” from renewables.

“Although strong short-term deployment is anticipated, capacity additions are still expected to fall short of the record-breaking 484GW of new solar and wind deployed in 2025. This is a key reason for the decline in global renewables investment expected in 2026, given the size of China’s domestic market,” the report concluded.

Pricing reforms last year are also expected to narrow profit margins and lower revenue certainty for renewable energy developers.

The short-term forecast for the US for new solar and wind deployment has also been downgraded due to the phase-out of tax credits and volatility surrounding Foreign Entity of

Concern rules and federal permitting procedures.

“Having plateaued from 2023 to 2025, low-emissions generation investment is consequently expected to decline in 2026,” the IEA said.

It pointed to US data for the second half of 2026 as a critical indicator to evaluate the resilience of solar and wind projects, given the heightened risks and removal of fiscal support.

A nuclear investment resurgence has also continued, exceeding $US80bn annually, with nearly 80 gigawatts of new nuclear capacity under construction across 15 countries.

A global pivot to net zero emissions may have also cooled in terms of momentum with the IEA noting the proliferation of sustainable finance and sustainability disclosure regulations had slowed.

“Asset managers, particularly in the United States, have distanced themselves from net-zero and sustainable finance initiatives, partly due to legal concerns about co-ordinated climate commitments,” the IEA said.

Carbon capture and storage, the technology relied up on by many oil and gas producers to lower emissions, also has an uncertain outlook with investment in 2026 revised down due to delays and “schedule revisions” by project developers.

“Compared with last year’s assessment, project timelines have been pushed back, shifting a

growing share of announced capacity into the mid‑2030s, and capital costs have risen above earlier expectations.”