Article by Patrick Commins courtesy of the Australian.

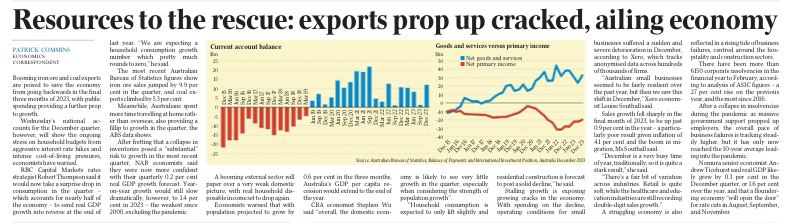

Booming iron ore and coal exports are poised to save the economy from going backwards in the final three months of 2023, with public spending providing a further prop to growth.

Wednesday’s national accounts for the December quarter, however, will show the ongoing stress on household budgets from aggressive interest rate hikes and intense cost-of-living pressures, economists have warned.

RBC Capital Markets rates strategist Robert Thompson said it would now take a surprise drop in consumption in the quarter – which accounts for nearly half of the economy – to send real GDP growth into reverse at the end of last year. “We are expecting a household consumption growth number which pretty much rounds to zero,” he said.

The most recent Australian Bureau of Statistics figures show iron ore sales jumped by 9.9 per cent in the quarter, and coal exports climbed by 5.3 per cent.

Meanwhile, Australians spent more time travelling at home rather than overseas, also providing a fillip to growth in the quarter, the ABS data shows.

After fretting that a collapse in inventories posed a “substantial” risk to growth in the most recent quarter, NAB economists said they were now more confident with their quarterly 0.2 per cent real GDP growth forecast. Year-on-year growth would still slow dramatically, however, to 1.4 per cent in 2023 – the weakest since 2000, excluding the pandemic.

A booming external sector will paper over a very weak domestic picture, with real household disposable income set to drop again.

Economists warned that with population projected to grow by 0.6 per cent in the three months, Australia’s GDP per capita recession would extend to the end of the year.

CBA economist Stephen Wu said “overall, the domestic economy is likely to see very little growth in the quarter, especially when considering the strength of population growth”.

“Household consumption is expected to only lift slightly and residential construction is forecast to post a solid decline,” he said.

Stalling growth is exposing growing cracks in the economy. With spending on the decline, operating conditions for small businesses suffered a sudden and severe deterioration in December, according to Xero, which tracks anonymised data across hundreds of thousands of firms.

“Australian small businesses seemed to be fairly resilient over the past year, but then we saw this shift in December,” Xero economist Louise Southall said.

Sales growth fell sharply in the final month of 2023, to be up just 0.9 per cent in the year – a particularly poor result given inflation of 4.1 per cent and the boom in migration, Ms Southall said.

“December is a very busy time of year, traditionally, so it is quite a stark result,” she said.

“There’s a fair bit of variation across industries. Retail is quite soft, while the healthcare and education industries are still recording double-digit sales growth.”

A struggling economy is also reflected in a rising tide of business failures, centred around the hospitality and construction sectors.

There have been more than 6150 corporate insolvencies in the financial year to February, according to analysis of ASIC figures – a 27 per cent rise on the previous year, and the most since 2016.

After a collapse in insolvencies during the pandemic as massive government support propped up employers, the overall pace of business failures is tracking steadily higher, but it has only now reached the 10-year average leading into the pandemic.

Nomura senior economist Andrew Ticehurst said real GDP likely grew by 0.3 per cent in the December quarter, or 1.6 per cent over the year, and that a floundering economy “will open the door” for rate cuts in August, September, and November.